We traveled to visit our parents-in-law. Whenever we are in town, I will make it a point to go to the local bookstore to pick up interesting books. I like to read books from local writers. We bought a few books. This book “Infallible Lighthouse” is easy to read and I finish it within a couple of days.

The book started to advocate dividend stocks such as utility companies and dividend growth stocks. The portfolio should consist of 70-80% of stable assets that create strong cash flow. It can be made up of treasury bonds, blue chips, REITS, and properties. The remaining 20-30% will be invested in growth stocks.

The basis of investment is to meet future expenditure requirements. First of all, you need to determine your annual expenditure. To do that, you need to keep track of all your expenses to understand the total expenditure. Based on your total expenditure, you can determine the return needed to meet your requirements. There is an external factor, the larger your portfolio, the lower the return is needed to meet your requirements. For instance, if your annual expense is S$120,000. A S$2,000,000 portfolio with 6% will be able to meet your expense requirement. If your portfolio size is S$12,000,000, a mere 1% return will be able to meet your expense requirement.

Quality of Cash Flow

The quality of cash flow is important as well, it needs to be sustainable. You cannot just invest your earned money in lousy companies just for high dividends. One possible reason that the dividend is high is because it is a value trap. The share price is beaten down and the yield looks high. You could be sacrificing your capital which is not a wise move.

Dividend Reinvestment

Some of the blue chips have DRIP (dividend reinvestment plan) investment schemes, which allow you to save the transactional costs. Fractional shares over the long run will add up to a single lot. If not, it is important to redeploy the dividend to invest back into the companies. Alternatively, you can invest the funds back to those companies that were weak last quarter. The most traditional investment is the round table investment. It could be investing in company A in January, investing in company B in February, investing in company C in March, and investing in company A in April. The cycle repeats itself.

Once you have created cash flow you have acquired the discipline to DCA and willpower to build up a portfolio. The cash flow will allow you to make mistakes and it won’t dent the portfolio. This gives you room to adjust and improve your investment strategy.

At the start of the year, you can estimate the annual dividend and interest/coupon from shares, bonds, and ETFs. At the end of the year, you can evaluate to compare the differences between estimated versus actual. For growth stocks or special investment situations, you need to evaluate at the end of the year whether the trigger happens. If the trigger happens, the share price rises. If it does, whether it is time to sell. If the trigger happens and the share price shows lackluster, does it mean your investment theory is wrong? It is important to understand the quantum of non-employment income because it can contribute to your liquid assets to buy more equities, bonds, and ETFs. It takes around 2-3 years to master a certain investment strategy. From there, you can adjust your investment strategy and fine-tune it. Investment strategy is highly personalized. It is curtailed to individual circumstances and investment goals.

How do I apply the theory from this book?

Firstly, our general household expenses not including mortgages will be around S$100,000 per annum. The net mortgage expenses work out to be around S$21,480 per annum. Let’s say we round it to S$120,000.

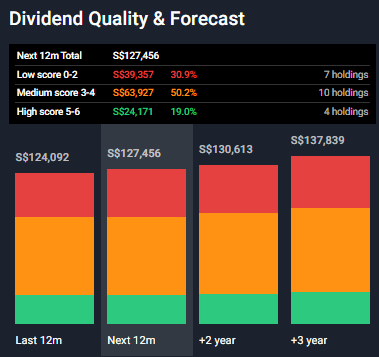

The dividend cash flow is enough to cover total household expenses. We will redeploy all employment income, side hustle income, and interest from P2P lending into the JC Fund portfolio. This compounding effect will create a stronger base and further reinforce the cash flow. Currently, the growth companies consist of around 18% of the portfolio while the remaining 82% consist of dividend stocks and ETFs. At the moment, we own a small TLT position which is around 2.8% of the portfolio.

We believe in 2-3 years we should be able to reach S$4m for JC Fund. The dividend should reach S$160k per annum by then.

Leave a Reply