Stone has two arms which are financial services and software. The financial services aim to provide the best financial operating system for Brazilian merchants. They provide financial technology solutions that empower merchants and integrated partners to conduct electronic commerce seamlessly across in-store, online, and mobile channels. Stone serves clients of all sizes and types that transact online, offline, or have an omnichannel sales approach. Stone serves many integrated partners, which use or embed Stone’s solutions into their own offerings to enable their customers to conduct commerce more conveniently.

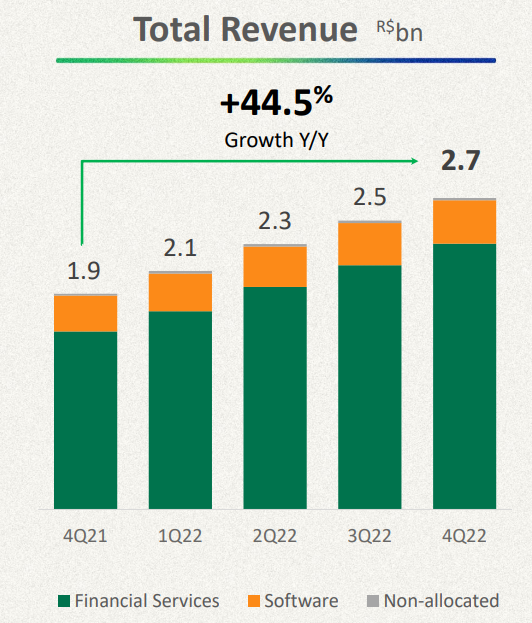

Revenue grew faster than TPV, doubling in 2022 to R$9.6 billion and up 44% y-o-y in 4Q2022 to R$2.7 billion.

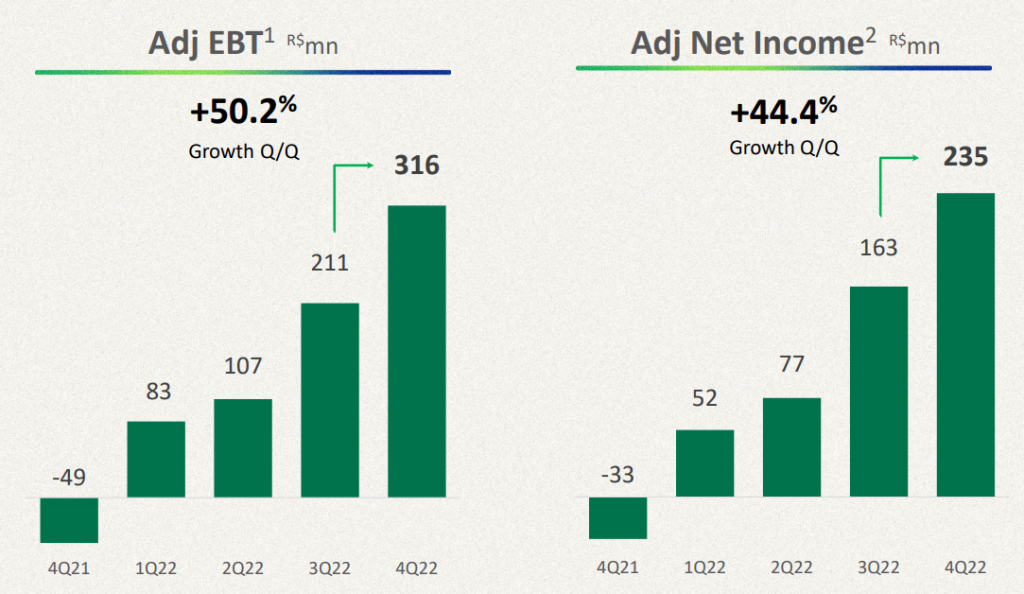

Adjusted EBT of R$316 million in 4Q22 with an adjusted EBT margin of 11.7%. The adjusted Net Income of R$235 million in 4Q22 which is a 44% increase q-o-q. The total adjusted Net Income for FY2022 is R$525 million compared to FY2021 which is R$ 84.7 million.

Financial Services has expanded its client base, new solutions, and higher take rate. The revenue is R$2.3 billion which is a 49.3% increase y-o-y from R$1.5 billion. Adjusted EBT is R$286 million with a 12.4% margin. For MSMB in 4Q22, the TPV has increased by 22.8% y-o-y R$81.9 billion compared to R$66.7 billion in 4Q21. The client base has increased by 48.3% y-o-y to 2.5 million merchants compared to 4Q21 which is 1.7 million merchants. The Take Rate increased by 50bps y-o-y to reach 2.21% in 4Q22 compared to 1.71% in 4Q21.

Initial pilots for full banking for micro clients under the offering “Super Conta Ton” is launched in 2022. The banking solutions include transactional products such as PIX, boletos, and tax payments. PIX-in tripled in 2022 to R$44 billion and increased 22% q-o-q in 4Q22, mainly driven by PIX P2M volumes. The banking client base reached 692,800 in 4Q22 compared to 492,000 in 4Q2021. MSMB deposits reached R$3.6 billion which is an 84.1% increase compared to R$2 billion in 4Q2021. ARPAC increases 77% y-o-y to R$45 per month per client. This is due to the Super Conta Ton.

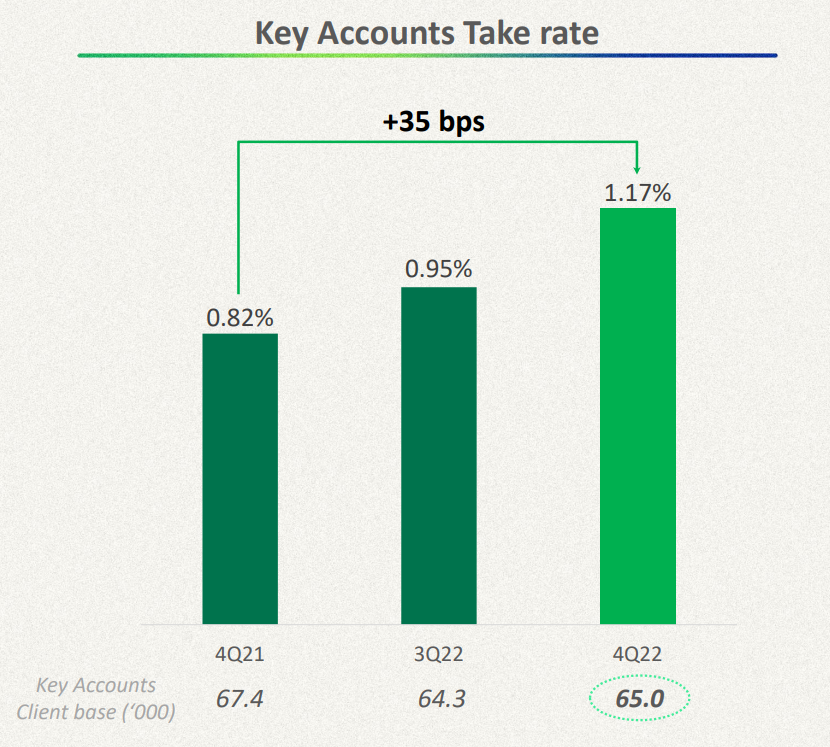

Its strategy to shift from sub-acquirers to Platform Services results in higher profitability. The Key Accounts Client Base decreases to 65000 in 4Q2022 compared to 67400 in 4Q2021 but the Take Rate increases to 1.17% in 4Q2022 compared to 0.82% in 4Q2021.

On the Software side

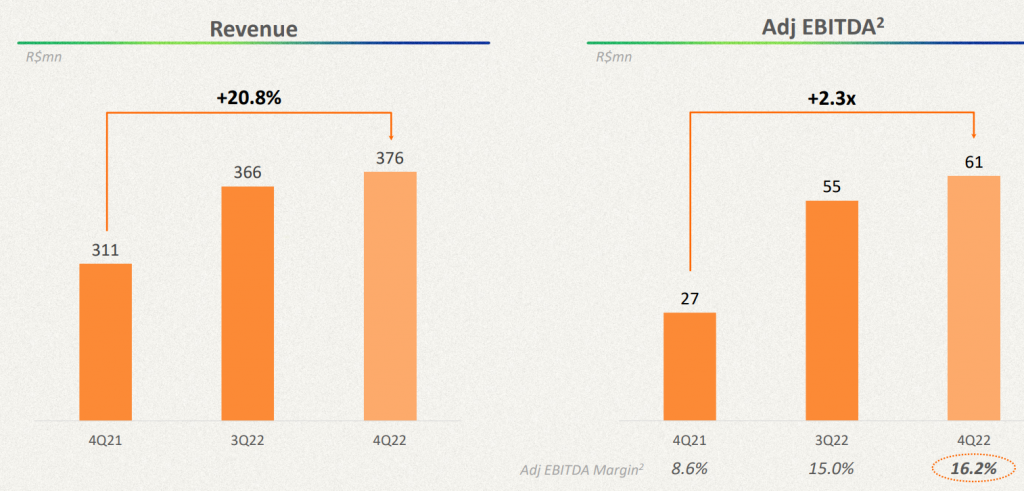

Software revenue growth of 21% y-o-y bringing it to R$376 million in 4Q22, bringing total revenue to R$1.4 billion in FY2022. Adjusted EBITDA Margin of 16.2% in 4Q22, up 120 bps q-o-q and 760 bps y-o-y, bringing it to R$61 million in 4Q2022 compared to R$27 million in 4Q2021. Integrated financial services platform to POS solutions in key verticals, which helps to increase cross-sell opportunities.

Core revenue grew by 23% y-o-y, driven by both increases in location and ticket sizes. Digital revenue increased by 4% y-o-y, due to the acquisition of Plugg.To, a marketplace integration hub that helps to offset weaker performance from ads and impulse businesses in the recent quarter. The integrated financial services platform to POS/ERP solutions in key verticals opens key cross-selling opportunities in FY2023. Stone is ready to pursue worthwhile M&A opportunities.

Cash

Stone has improved cash generation throughout the year, culminating in the strongest quarter over the last year. The adjusted net cash increased by R$385 million q-o-q and R$1.2 billion y-o-y to R$3.5 billion in 4Q22.

Conclusion

I like the turnaround story for the business. It has made some mistakes in the past and it is trying to be more focused on its core business. We will continue to stay invested in this business and will monitor its future quarters’ performance.

Refer back here to the past quarter’s results.

Leave a Reply